What is Private Car Insurance?

Private Car Insurance is a contract between a car owner and an insurance company in which the owner pays premiums and the insurance company protects him from financial loss in the event of a car accident or other unforeseen event. The damage caused by the collision might be to his own vehicle or to someone else’s car or property, for which he will be held responsible. Both of these damages are covered by car insurance in India.

Most vehicle insurance firms have agreements with manufacturers to provide insurance at the time of purchase.

Why do you need a Car Insurance?

Car insurance is vital to any driver. It doesn’t matter if you’re a new driver or have been driving for years, car insurance provides several other benefits that are worth considering. Whether it’s the peace of mind knowing your vehicle can be replaced in an accident or being able to drive without having to worry about every scratch and dent on your car, there are many good reasons why you should get car insurance.

Any or all of the following are possible consequences of a car accident:

Third party insurance is a compulsory legal requirement, and every car owner must have this. As per law, the registered owner of the vehicle may have to pay compensation for (B) and (C) if the vehicle is responsible for an accident. Since not everyone can afford such compensations, it becomes necessary that they take out third party insurance which pays for these accidents.

Own damage cover insurance is optional insurance that covers the cost of repair to your own vehicle in case of (A). If the car is acquired with a loan, the financier will want such insurance coverage because the vehicle purchase was financed by the financier.

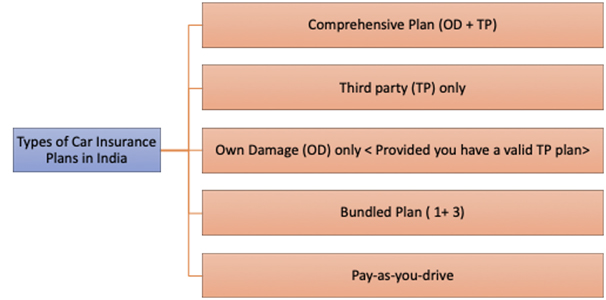

What are the types of plans available?

There are primarily two types of car insurance policies.

Third party Liability Insurance

According to the Motor Vehicles Act, 1988, it is mandatory for Indian drivers to have valid third-party liability insurance to drive your car on the Indian roads. It covers you against any claims made by a third-party to pay for the treatment, damage or repair if your car damages him or his vehicle or property during an accident. It covers all your legal liabilities for any third-party damages done to a third-party vehicle, property or a person. There is no coverage provided to any damages to your own car.

Assume you collided with another vehicle while learning to drive. Now, you have a legal responsibility to compensate that car’s owner for his losses. This insurance will cover that car’s repair cost for you.

Comprehensive Insurance

The comprehensive insurance covers any damage or loss to your vehicle, as well as any third-party liabilities. It covers the car against accidents, theft, fire or any other natural calamity.

Let’s say your car was engaged in a collision. This insurance will cover the cost of your car’s repairs as well as any third-party losses or damages, if any to any third-party vehicle, etc.

Other types of car insurance plans available in India:

1. Standalone Own Damage

The Standalone Own Damage Plan provides coverage against own damage. This comprises losses and damages resulting from crashes, natural disasters, thefts, and fires. However, you can opt for a standalone Own Damage Plan ONLY if you have a valid Third-Party only insurance plan and not otherwise.

2. Bundled Plans (1+3)

The IRDAI has mandated from September 1, 2018, that all new cars need to have a minimum 3 year third-party coverage. So, you can purchase a Bundled Car Insurance Plan (1+3) i.e. you would get 1 year own damage coverage along with the mandatory 3-year third-party coverage. After completion of the first year, since your third-party coverage would be valid for 2 more years, you can opt for a standalone own damage car insurance plan.

3. Pay as you drive

Pay as you drive (PAYD) is a relatively new form of car insurance in which premiums are dependent on how much the vehicle is driven over the course of the policy term. The vehicle-year is replaced by a vehicle-kilometer or vehicle-minute as the unit of exposure. In simple terms, you pay more if you drive a lot, and you save more if you drive less.

| Policy Types | Own Damage | Legal Liability (third Party Insurance) | Scope |

|---|---|---|---|

| Liability Only Policy Annual | No | Yes | Provides Third-party liability coverage for a year. |

| Liability Only Policy 3 Years | No | Yes | Minimum Requirement for new Vehicles. Provides Third-party liability coverage for 3 years. |

| Package Policy Annual | Yes | Yes | Provides comprehensive coverage for a year. |

| Package Policy Bundled (1 plus 3) | Yes | Yes | Annual cover for Own Damage and 3 years Third Party Insurance – For New vehicles |

| Stand Alone Own Damage Policy | Yes | No | For giving Own damage cover for after the expiry of one year cover in a bundled policy or a liability only policy. |

| Fire & Theft only Policy | Yes | No | To have cover own damage to the vehicle due to Fire and Theft and other related risks |

| Fire and Theft only policy with legal liability | Yes | Yes | To have cover own damage to the vehicle due to Fire and Theft and other related risks along with legal liability (third party) |

PA Cover

Accidents can result in serious injuries, impairments, and, in the worst-case scenario, death. Personal accident (PA) coverage is a feature of car insurance that is available to the owner-driver. It is issued in the owner’s name. However, the policy may only be used if the owner has a valid driving license.

The Insurance Regulatory and Development Authority of India has set a personal accident coverage limit of 15,00,000 INR and is required regardless of whether you choose third-party or comprehensive insurance. It can be taken along with your third-party or comprehensive car insurance plan or even separately.

In case of death of the owner, the nominee will get the following coverage as per the table:

| Coverage For | Loss of 2 limbs OR 2 eyes OR 1 limb and 1 eye |

| Loss of 2 limbs OR 2 eyes OR 1 limb and 1 eye | 100% |

| Loss of sight or 1 eye or 1 limb | 50% |

| Permanent Total Disability | 100% |

Difference between TP and Comprehensive Car Insurance Plans:

So, technically there is a difference between third-party and comprehensive car insurance plans:

| Particulars | Third-Party (TP) Car Insurance | Comprehensive Car Insurance |

|---|---|---|

| Coverage | Provides coverage to any third-party legal liabilities caused to any vehicle, property or person. | Provides both Own Damage (OD) + third party (TP) coverage |

| Add-on Covers | There can be no additional benefit added along with the mandatory TP plan except personal accident cover. | The coverage of a comprehensive plan can be extended using various additional benefits such as zero depreciation, etc. |

| Need | Mandatory as per the IMV | Optional (on TP is mandatory) |

What is covered under Car Insurance?

Here is a list of the things covered under comprehensive Car Insurance.

- Damage – Car insurance covers any damage to your vehicle as a result of an accident or natural disaster under own-damage and comprehensive insurance plans.

- Third party property damage – Car insurance covers any damage to a third party property caused by your vehicle in the event of an accident or natural disaster.

- Injury – Car Insurance covers any injuries severed by the vehicle’s owner-driver in the event of an accident or natural disaster under PA cover.

What is not covered under Car Insurance?

Here is a list of the handful of things not covered under Car Insurance, unless specifically mentioned

- Issues related to the general wear and tear of the car.

- Mechanical failure and wear of specific parts such as Tires.

- Damage suffered outside the country or during a war.

- Damage caused by a driver who does not have a valid driver’s license or is intoxicated.

- Damage occurred when the vehicle was being utilized for reasons not specified in the insurance policy

| Type of Exceptions | Applicable to | Remarks | ||

| Own Damage | Legal Liability (third Party Insurance) | Benefits (PA Cover only) | ||

| Consequential Loss | Yes | Yes | Yes | (financial loss – like engaging a taxi since the vehicle met with an accident) |

| Depreciation | Yes | (reduction in value of the vehicle due to accident and repairs) | ||

| Depreciation on parts / materials ( when the vehicle is being subjected to repairs of the damages due to the accident | Yes | Depreciation as per the age of the vehicle for metal parts, 50% on rubber/ nylon etc. parts , 30% on fiber parts, 25% on painting materials. | ||

| Wear & Tear | Yes | |||

| Mechanical / Electrical Break down / Failures / breakages | Yes | |||

| Damages to tyres unless the vehicle met with an accident( damage only to the tyre even due to accident is not payable) | Yes | Even when the tyre is damaged along with the vehicle’s other damages, only 50% is payable. | ||

| Driving under the influence of intoxicating drugs or liquor | Yes | Yes | ||

| Intentional self-injury, suicide, attempted suicide physical defect or infirmity | Yes | |||

| Hire or reward | Yes | Yes | Yes | |

| Driving by a person not licensed as per the drivers clause of the policy | Yes | Yes | Yes | |

| Carriage of Goods (other than samples & personal luggage) | Yes | Yes | Yes | |

| Organized racing, pace making, speed testing, reliability (relating to motor sports) trial | Yes | Yes | Yes | |

| Any purpose in connection with motor trade (that means when the vehicle is in the custody of a dealer / repairer / financier/ used car dealers etc.) | Yes | Yes | Yes | |

| Accidents / loss outside the geographical area. | Yes | Yes | Yes | |

| Liability due to a contract | Yes | Yes | Yes | |

| A few other perils like nuclear / war like related (please refer to the appropriate wording. | Yes | Yes | Yes | |

| Any extension of damage or further damage at the accident / breakdown site if proper precaution is not taken or driven before necessary repairs | Yes | |||

What are the add-on covers available by paying an extra premium?

Assume you purchased car insurance to safeguard your prized new vehicle. However, you somehow managed to damage its engine, for which the insurance company does not provide coverage. Isn’t that going to be terrible? This is when add-covers come in handy.

By acquiring add-on coverage, you boost the efficiency of your vehicle insurance. By paying a slightly more premium amount, you are providing extra coverage to your travel companion.

Now, let’s have a look at the most common types of add-on covers available in India.

Engine Protection – Non-accidental car damage is not covered by standard car insurance. This add-on safeguards the engine, which is the most vital component of your prized travel buddy. Oil spills, water intrusion, and engine technical breakdown are all covered under the policy.

Tip: It should be noted that this add-on is not usually compatible with vehicles older than five years. This add-on comes most handy if you live in an area prone to waterlogging.

Zero Depreciation – This add-on, also known as nil depreciation or bumper to bumper car insurance, bears the weight of depreciation on your vehicle’s parts and assures a greater claim amount.When your car reaches the 6-month mark, its value begins to depreciate, and even a minor bump might send your car to the workshop. The danger is heightened by the fact that luxury car parts might cost twice or three times as much as standard ones. But, if you have this add-on coverage, you will get the full amount of your claim without any deductions for depreciation.

Tip: Some insurance providers provide two zero depreciation claims, whereas the majority provide limitless depreciation claims.

- No Claim Bonus Protection – If you haven’t filed any claims in the previous year, you get a discount on your annual premium. This discount grows each year you go without filing a claim and then vanishes the moment you do. For the first year, the NCB discount rate is 20%, increasing to 50% for the fifth year in a row. This add-on assures that you get an NCB discount year after year, even if you file claims.

- Roadside Assistance – Your vehicle might break down at any time. Let’s say you’re on a lengthy journey and your car suddenly stops in the middle of the highway, leaving you stranded. Here’s where this add-on comes in handy. With a single phone contact with the insurance firm, a mechanic will be dispatched to your aid. This add-on covers on-the-spot roadside help.

- Return to Invoice – Your new car begins to depreciate and lose value the instant you drive it out of the dealership. In the event of complete or constructive loss or theft of the car, this add-on assures a claim for the invoice amount.

Tip: Depending on the insurance carrier, this add-on is only available for cars that are less than three to five years old.

- Daily Allowance – Let’s say you have given your car to the garage for maintenance and repair and the process is going to take around 3 days. With your car not available, you have to rent or hire a car to finish your daily tasks. This add-on gives daily travel allowances if your car is in the insurance company’s network garage for more than two days.

Other add-ons:

- Passenger Cover – Some standard car insurance policies may not cover injuries sustained by passengers in the covered vehicle in the event of an accident or natural catastrophe. This add-on will take care of it for them.

- Consumables Cover – Frequently, you will be charged for consumables used during the repair of your vehicle. It’s taken care of by this add-on. It protects you from these kinds of out-of-pocket costs. It is usually not applicable to cars older than five years.

- Tire Protection Cover – This add-on protects your covered car’s tires from non-accidental damage, as the name implies. Puncture, tire rupture, and bulging are just a few of the problems that might occur.

- Replacement Key Cover – Assume you’ve misplaced your electronic vehicle key and don’t have a spare. This add-on covers all costs associated with key replacement and lock-set repair.

- Loss of Personal Belongings – This add-on provides coverage to the thief or loss of personal belongings in the insured car.

| Type of Add-on Cover | Type of Cover | Remarks |

| Nil Depreciation Cover | OD | To get a claim without depreciation on parts etc. |

| Engine Protector | OD | To cover internal damages due to aggravation of loss |

| Tyre Cover | OD | To get claim even if the tyre alone got damaged |

| Key Replacement Cover | OD | To get a claim for replacement of related locks and keys when the key is lost |

| Hydrostatic Cover | OD | To cover engine damage due to water entry into engine |

| Consumables Cover | OD | To cover the cost of consumables when the vehicle is getting repaired |

| Invoice Cover | OD | To get the invoice value of the vehicle when the vehicle becomes a total loss |

| NCB Protector for windshield Cover | OD | No claim bonus earned is completely withdrawn when a claim is made. However with this add-on cover, the NCB will be protected even if a claim is made |

| NCB Protector for any Claim | OD | As above |

| NCB Protector Repair of Glass / Fiber / Plastic / Rubber | OD | As above |

| Road Tax Cover | OD | To get prorated portion of the road tax paid in the event of total loss |

| Loss of Baggage | Benefit | Loss of personal belongings are excluded. This add-on cover would cover the same |

| Spare Car or Cash in lieu of Car | Benefit | To provide cash for repairs rather than repairing the car. |

| Enhanced PA Cover | Benefit | To get a claim based on a specific scale for physical injury/death incurred by the car’s owner-driver. |

| Hospital Cash | Benefit | To cover incidental expenses whilst being in hospital due to accident injury |

| Ambulance Charges Cover | Benefit | Contributes to the cost of an ambulance journey in the event of an injury during a car collision. |

| Medical Expenses Cover | Benefit | To pay for medical expenses incurred as a result of a car accident injury. |

| Outstation Emergency | Benefit | To provide assistance in the event of an emergency, such as an accident or a car breakdown |

| Loss of DL or RC | Benefit | Incidental expenses in getting a duplicate |

| Roadside Assistance | Benefit | To get support at the accident site for protection and towing of the vehicle |

| Legal Liability towards Paid Drivers and cleaners employed in connection with operation and/or maintenance of motor vehicles under the EC Act, FA Act and Common Law – Wider Legal Liability. | Legal Liability | This is mandatory |

| Legal Liability to employees of the insured travelling in and /or driving the employer’s vehicle. | Legal Liability | This is mandatory |

| Compulsory PA cover for Owner Driver | Benefit | This is mandatory |

| PA Cover for Insured and any named person other than Driver / cleaner | Benefit | To provide cover for insured persons other than driver and cleaner traveling at the time of an accident. |

| PA cover for unnamed persons equal to the registered seating capacity of the vehicle excluding Insured, driver and cleaner. | Benefit | To provide cover for unnamed passengers traveling at the time of an accident. |

| PA cover for paid driver(s), cleaner(s) and Conductor(s) | Benefit | To provide cover for the driver, cleaners and conductors traveling at the time of an accident. |

| Increased Towing | OD | To cover towing charges of the insured car. |

All add-ons are not provided by all plans and it varies from insurer to insurer. You need to check your plan and its add-ons before choosing one!

Types of Car Insurance Claims

There are mainly two types of car insurance claims:

- Own Damage Claims: Assume you’ve been in a collision with your vehicle. Own Damage Claims pay for the damage to your own car that occurred as a result of the collision.

- Third-party Insurance Claims: Let’s say your car was engaged in a collision. Third-party insurance claims cover the damage your vehicle caused to a third party and their property in a collision or natural disaster. The claim procedure is completely different in this case. You need to file your claim with the Motor Accident Claims Tribunal (MACT). The court would hear from both sides and decide if you need to be compensated.

Claim procedure for your own damage of your car:

Car insurance can either be cashless (at a network garage) or on a reimbursement basis. Here is a step-by-step procedure for claiming car insurance under those subdivisions.

For Cashless Claim:

- You need to go to an authorised garage for a cashless claim.

- File a claim with the insurance (contact them, record a claim online or through the app), or the garage will take care of it.

- A surveyor would inspect your car at the garage before starting the repair work and would provide you with an approval based on the estimate of the repair work provided by the garage.

- Once the cost is approved, the garage would complete the repair work.

- The insurance company would pay the bills directly to the garage.

- The remaining amount needs to be paid by you (that has not been approved by the insurance) in order to take possession of the car.

For Reimbursement Claim:

- File a claim with the insurance company (call them, log a claim online or through the app) before the repair work is done.

- A surveyor would inspect your car at your home or in a non-network garage, or via videos/pictures through their mobile application, etc.

- Then the surveyor would provide you with an approved amount of the claim.

- Once the claim is approved, you need to get the repair-work done at any garage of your choice

- Pay the entire money upfront to repair your car.

- Then, you need to send the claim form along with the original repair bills, your KYC documents, policy document, and bank account information to the insurance company for the amount to be reimbursed along with the surveyor’s approval.

- In case of an accidental claim, you must file a Motor Collision Report at the local police station.

The following are the documentation that must be submitted to the insurance company:

- A copy of your insurance policy, valid driving license, car’s registration and tax certificates, etc.

- A copy of the filed FIR or an MCR (Motor Collision Report) in case of an accidental claim

- Duly filled and signed claim form along with your KYC documents.

In case of a reimbursement policy, these additional documents are required:

- An estimate of the repairs as provided by the surveyor

- Original receipts for the repair-work

- Your bank account details for the money to be credited.

Car Insurance Renewal procedure

For continuous coverage, every vehicle owner must renew their insurance before the due date. People should be aware that if they do not renew their car insurance by the due date, the coverage will immediately expire. As a result, the policy would terminate the insurance coverage provided under the car insurance policy. If you discover that your insurance has expired or is likely to expire within a few days, you must renew it immediately.

Here is a step-by-step procedure for the renewal of car insurance:

- Fill up the information about your vehicle.

- Choose your preferred insurance plan

- Fill up the information of your prior insurance policy

- Select add-ons if you wish

- Make the payment using a credit or debit card or via net banking.

The policy document would be emailed to the registered email id. Alternatively, it could also be done offline.

Top 6 Tips on avoiding claim rejection

Let’s assume you were in an accident and severely wrecked your new car. The worst thing that can happen now for you is to get your claim denied. And believe us when we say that it happens very frequently. But let’s be honest: Most of the time, insurers exploit legal loopholes and provisions in their policy agreements to avoid paying sums guaranteed, but in a surprising number of instances, the responsibility and blame lie with the consumers.

With that established, let’s go over a few tips that will help you avoid claim rejection.

- Reveal all information accurately

- Make sure you pay your premiums on schedule

- Make sure you file your insurance claims as soon as possible

- Fill up your own insurance application

- Accept any survey that may be necessary, for reinstatement or a new insurance plan

- Examine the policy paper in detail once you receive it to check if all information has been accurately captured!

Once you keep these aspects in mind, chances are you will get your claim very easily!

Dos and Don’ts of Car Insurance

Here are a few Dos and Don’ts when it comes to purchasing car insurance.

| Dos | Don’ts |

| Fill out the proposal form yourself. | Don’t forget to renew your insurance coverage. |

| Make a copy of the entire offer for future reference. | Don’t forget to ask about the proper procedure when buying a used car with insurance. |

| Read the policy Terms and Conditions. | Make no misleading statements regarding the real use of the car you’re insuring. |

| Inquire about any available add-on coverings and select the one that most matches your needs. | |

| Provide the insurance company with up-to-date documentation for verification. |

Latest news on Motor Insurance

- Bengal will issue smart cards with QR codes and driver’s licenses.

Vehicle and driver’s license smart cards will now have a QR code.

When a QR code on a smart card is scanned, it displays all pertinent information about a vehicle, such as registration date, where it was registered, the owner’s fitness certificate, and whether the vehicle’s insurance is still current.

The code on a driver’s license will disclose if the license is legitimate and whether the bearer has a history of breaking traffic laws. The QR code will have a chip integrated into it and will be put below the portrait of the licensor. - Comprehensive insurance may increase the cost of new cars by as much as 10%.

Buying a new car might cost up to 10% extra in the coming months, as India’s insurance sector is being compelled to rethink policy designs and existing risk models of motor coverage as a result of an order issued by the Madras High Court last week.

Frequently asked questions

What is Insured’s Declared Value (IDV)?

IDV is the vehicle’s Insured Declared Value, and it is the maximum value insured by the insurer if the car is stolen or there is a complete and total loss.

In a nutshell, IDV refers to your vehicle’s current market worth. It’s generally calculated using the manufacturer’s suggested retail price for the model and variation of the car (including optional equipment) at the start of the policy. Depreciation amounts are adjusted against IDV every year.

How does the No Claim Bonus (NCB) discount work?

While everything else increases in price, your vehicle insurance provides you with a unique benefit by allowing you to minimize your premium. You may be curious as to how it works.

It’s almost like a reward system, really.

- If you haven’t made any claims during your first policy year, you’ll get a 20% NCB discount.

- As a result of your second straight year of making no claims, you continue to receive an additional 5%.

- This rate of discount will increase to 50% in your sixth year.

To summarize, the better you prove to safeguard your car, the less you have to pay as a premium.

How can I reserve my existing No Claim Bonus discount (NCB) for my new car?

As long as you are the policyholder for both cars, you can transfer your existing No Claim Bonus discount to another car. All you have to do now is terminate your existing insurance and wait for your old insurance company to send you an NCB retention letter. To receive the discount, you must now submit the same to the new insurance carrier.

An insurance company will require the following documents to issue a retention letter.

- A letter requesting the termination of a policy.

- Original copy of the policy.

- Original insurance certificate.

If you are selling your old car, you’ll need to present the following papers in addition to the ones stated above:

- Form 29: Notice of Transfer of Ownership

- Form 30: Application for Intimation and Transfer of Ownership

- A photocopy of the registration certificate book with the new owner’s name.

- Proof of sale and delivery to the new owner.

What is the procedure to cover Electrical and non-electrical accessories?

Car gadgets, both electrical and non-electrical, play an essential role. These extras will allow you to fully personalize your ideal car. If you live in a region where theft is common or where natural disasters are common, it may be a smart idea to insure these items.

Standard car insurance usually covers the primary body of the vehicle and covers claims for accidental damage to it. As a result, if one of your expensive electrical or non-electrical gadgets is stolen or destroyed, you will not be reimbursed.

The process for covering these accessories is to get an add-on that protects those who keep your four-wheeled beauty safe and comfortable.

How can I get an additional discount on my premium?

Here are a handful of tips that help you receive an additional discount on your premium:

- Establish an optimal IDV. You should choose a value that is neither too high nor too low. As a result, you must pay a relatively small sum, but the claim amount is adequate for you.

- Raising claims for trivial concerns is one of the most typical mistakes people make. If you continue to file claims, you will lose your NCB bonus. Instead, pay for minor claims and ensure that you receive the NCB discount every year.

- Some insurers provide discounts for cars that have anti-theft equipment fitted. The gadget should, however, be approved by the Automotive Research Association of India.

- Drive carefully. If you haven’t filed a claim in the previous year, you are eligible for an NCB discount. For the first year, the discount is 20%, increasing to about 50% for the fifth year in a row.

- If you want to maximize every claim opportunity, No Claim Bonus Protection is a must-have add-on to keep your NCB bonus amounts consistent year after year.

- Check to see whether your car insurance is up for renewal. You don’t want to wait until the last minute to renew your policy since if you fail to renew it during the grace period, you may be required to get new coverage.

What is an Owner/Driver Personal Accident Cover?

Owner/Driver Personal Accident Coverage is a service provided by vehicle insurance companies that covers injuries, lifelong disabilities, and even the death of the insured car’s owner-driver in the event of an accident or natural catastrophe.

What is an Unnamed Personal Accident Cover?

This is Personal accident cover for unnamed passengers which could include family members or friends traveling with you at the time of an accident.

What is Driver cover?

Under the Driver cover policy, the insurance company compensates for injuries, lifelong disabilities, and even the death of the insured car’s driver in the event of an accident or natural catastrophe.

What is a Third Party cover?

Mandatory under Motor Vehicles Act, 1988, Third party cover provides coverage against any claims made by a third-party to pay for the treatment, damage, or repair if your car damages him or his vehicle or property during an accident.

What is covered under the Own Damage Section of the policy?

The Own Damage Section of a standard insurance policy provides coverage against theft or damage to the insured car.

How to check if my policy is genuine?

All genuine insurance firms have a QR code app, according to the Insurance Regulatory and Development Authority of India’s (IRDAI) stringent guidelines. The QR code confirms the policy’s authenticity because clients receive regular updates on their insurance policy via the app.

Is my car covered outside India?

No. Standard Indian car insurance typically does not cover vehicles outside the geographical location of the country.

Is my car covered inside a workshop or a hotel?

Yes. Standard car insurance policies cover your car from any damage or theft even inside a workshop or a hotel.

How does financier hypothecation work?

The hypothecation in vehicle insurance is done in favor of the bank from whom you obtained the loan. The car will stay in the bank’s possession until the whole debt is paid off. Until you have complete ownership of the car, the insurance company will put a notation of the loan on the insurance policy paperwork.

What is the role of an Ombudsman?

The Ombudsman’s goal is to resolve any difficulties that arise during the settlement of such claims. The primary objective of implementing an Insurance Ombudsman is to offer an efficient and fair resolution of policyholder concerns.

How does Grievance Redressal work?

The purpose of Grievance Redressal is to guarantee that all policyholders are treated equally at all times and that all policyholder inquiries, requests, and complaints are handled with politeness, accuracy, and speed.